Private credit is where a non-bank lender provides loans to companies, typically to small and medium size enterprises that are non-investment grade. Private credit can serve as a diversifier in a private markets portfolio as debt is less correlated with equity markets. Plus, it allows for a shorter J-curve due to the periodic income component from repayments.

Table of Contents

Private credit in a nutshell

- Target companies. Though the company stage varies, private credit managers generally lend to non-investment grade, small- and medium-sized enterprises.

- Investment type. Direct loans – which are senior in the capital structure – with bespoke terms and floating-rate coupons.

- Value-add operations. Unlike private equity, there is no involvement in the running of a target company. Direct value-add comes mostly from restructuring expertise.

- Source of return. Private credit firms charge a floating rate spread above the reference rate, allowing the fund and investors to benefit from increasing interest rates

What is Private Credit?

As regulatory changes have led to traditional lenders – such as banks – stepping away from lending to middle-sized enterprises, private credit managers have seized the opportunity to enter the market, lending to small and medium size enterprises that are non-investment grade.

Target companies are often sourced from a credit manager’s proprietary network. The manager has the flexibility to set its preferred lending terms, typically arranging for protective covenants and collateral to protect against defaults.

Returns are achieved by charging a floating rate spread above the reference rate, allowing the lender and investors to benefit from increasing interest rates. Unlike private equity, private credit agreements have a fixed term, meaning that the “exit strategy” for an investment is pre-defined.

Types available

Private credit is available as:

- loans

- bonds

- notes

- private securitisations (a type of asset-backed financing structure)

This page focuses on loans only.

What do typical loans look like?

Asset-based finance

When a business borrows money secured against the value of assets it owns.

Learn more about asset-based lending.

Cash flow finance

When a business borrows money secured against its expected cash flows.

As a result, the business’s equity can be considered the collateral (security) of the loan.

Trade finance

This allows borrowers to buy specific goods in both domestic and international markets.

The finance is often transactional, provided only for specific shipments of goods and for specific periods of time.

The debt is secured against the goods being financed.

Real estate finance

When a business borrows money secured against an underlying real estate asset (an investment in property, for example).

Infrastructure debt

Used to finance long-term infrastructure or industrial projects.

The borrower repays the debt using the cash flow generated from the project the lender has financed, once complete.

Rescue finance

Loans provided to companies that have filed for bankruptcy or are very likely to do so in the near future.

Venture debt

Also known as venture lending, this is a loan provided to early-stage venture-backed companies that enables them to proactively finance growth.

How do Private Credit managers add value?

Proprietary network. A private credit firm’s proprietary network of target companies and entrepreneurs allows them to screen for the best opportunities based on demand, geography, market position, cash flows and management.

Risk management. Enhanced due diligence is fundamental in screening out risky borrowers. Private credit managers will leverage their strong market expertise to provide robust private credit analysis.

Structuring expertise. In case of a default, managers can deploy the required resources to assist companies in the bankruptcy process, helping to extract maximum value for the fund.

WHY INVEST IN PRIVATE CREDIT?

Private credit can be a powerful complement to traditional fixed income strategies, offering incremental income generation, potential resilience, return enhancement, and diversification.

Income generation. Over the past decade, the asset class has generated higher yield than most other asset classes, including 3-6% over public high yield and broadly syndicated loans. Borrowers have been willing to pay a premium for the certainty of execution, agility and customization that private lenders offer.

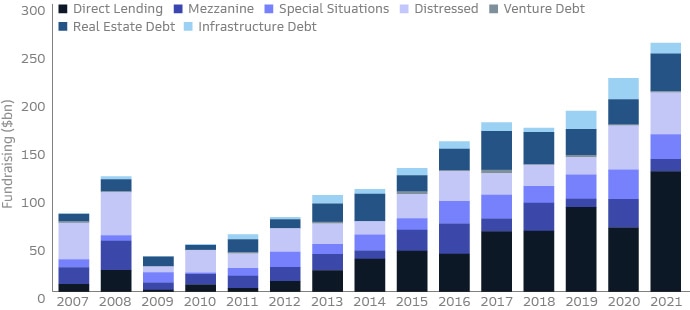

The Universe of Private Credit Strategies Has Been Expanding, Diversifying

Resilience. Private credit has historically maintained loss ratios that are lower than those of high-yield fixed income instruments. Deep access to company records received by private lenders enables stronger due diligence and documentation than may be the case in public markets. The ability to select investments without the need to manage to a benchmark can be a potential downside mitigant in an environment of increased dispersion, slowing growth, tightening monetary policy and headwinds to profitability. Furthermore, private credit typically features a single entity lending to a borrower. This can make for quicker and more efficient workouts—and potentially greater recovery—in case of default, compared to publicly syndicated debt placements that feature multiple lenders with competing priorities.

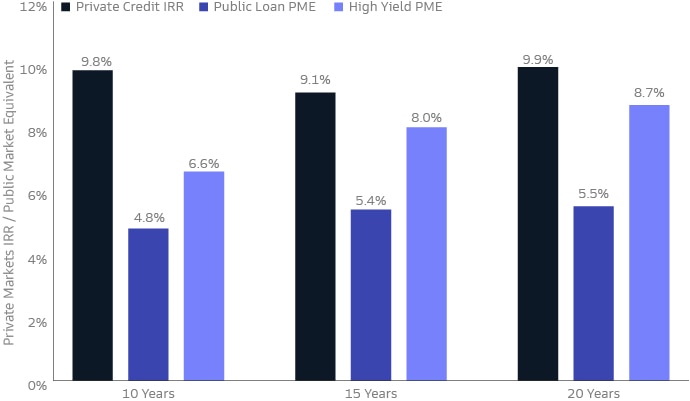

Potential return enhancement. Aided by the yield premium and resilience dynamics, private credit has outperformed public loans over the past decade, having delivered 10% annualized returns compared to an annualized 5% for public loans.1 In a rising-interest rate environment, private credit may find its floating rate nature a further advantage. Private credit instruments are typically tied to floating rates (such as SOFR). When interest rates rise, those increases are automatically reflected in the private credit coupon. This dynamic makes floating-rate debt less sensitive to interest rates compared to fixed-rate bonds, which typically lose value as interest rates rise.

Diversification. Some private credit strategies are most directly exposed to the economic health of corporate borrowers, others to the consumer, others to real assets. Some strategies, such as performing corporate and real asset credit, tend to move with the economic cycle. Others, such as distressed and opportunistic, may be more counter-cyclical, finding more attractive opportunities when the economy is challenged. Some specialty credit strategies are less sensitive to the cycles of the broader economy.

Comparison of Overall Performance1

Evolution of the Asset Class

The private debt market has grown more than six-fold since the Global Financial Crisis of 2007-2008, with senior lending strategies having experienced the most robust growth. Today, the private credit market stands at $1.2 trillion.2 Part of this growth has been driven by increasing barriers to entry in certain market segments. For instance smaller companies have found it more challenging to access public markets as the average bond and syndicated loan deal sizes have grown.

Much of the growth in demand for private credit solutions, however, has been driven by the unique value proposition that private lenders can offer borrowers. Private lenders are becoming preferred financing partners due to their sophistication, flexibility, certainty of execution, and the critical support they can offer to borrowers in challenging environments, as evidenced most recently through the COVID-19 pandemic. Some strategies also focus on assets or structures too complex for typical traditional lenders to underwrite, relying on complex approaches to properly evaluate and manage risks.

The growth of the asset class, buoyed by investor interest, has also helped it expand its scope. While historically private lenders focused on middle-market companies, the recent growth in fund sizes has made it possible to also finance larger deals while maintaining prudent fund diversification parameters. It has also enabled innovative approaches to better meet borrower needs— such as the emergence of unitranche transactions, in which a lender issues a single credit instrument, rather than a more complex capital structure that would subdivide the borrowed amount into junior vs. senior tranches of debt.

Finding the Right Partner

With a variety of strategies, the dispersion of results can be wide. Even within a strategy, the range of outcomes can vary based on the skill and experience of the manager. This makes finding the right partner critical. Critical items to consider include the types of borrowers and assets each manager is lending against, their position in the capital structure, the terms and protections they negotiate, their experience and track record in investing through multiple cycles, and their expertise in managing through stressed and distressed situations.

What are loans used for?

Borrowers use these loans for a variety of purposes, such as:

- funding plans for acquisition or expansion

- improving working capital

- refinancing

Among the most popular borrowers are small and medium-sized businesses.

However, many firms cater to larger businesses.

Benefits

Growth

Although your business may choose to sell equity as a way of financing its growth, if you’re established and profitable you might want to avoid the surrendering of control that equity finance often brings.

Consequently, private credit gives you a wider and more competitive choice of debt finance for expanding and scaling up your business.

For many smaller and mid-sized firms that are looking to be more ambitious in their growth and development, this can often be the key to unlocking their potential.

Flexibility

Some lenders have strong restructuring skills that allow them to provide operational support in challenging economic environments (such as COVID-19).

Direct lending is also well suited to supporting firms in their recovery efforts, and beyond, thanks to its bespoke and adaptable structures.

With many of the UK’s small and mid-sized companies having taken out emergency loans to survive the immediate impact of COVID-19, ‘debt overhang’ (a debt burden so large that it stops the business taking on more) is a key challenge and risk, requiring careful planning and consideration as the economy recovers.

Funded by direct lending, your business may be better able to withstand a contracting economy and take advantage of opportunities for expansion.

Deals are generally structured with a large proportion of ‘bullet repayments’ (when you pay back the finance in one lump sum at the end, rather than in instalments).

This gives you access to the capital you need to invest in growth, rather than having to meet immediate obligations to repay debt.

Refinancing

Private lending may also be suitable if your business is currently funded through bank lending and has a strong opportunity to grow.

While it may cost you more, it would allow you to replace an existing loan with a structured lending product whose repayment terms are more flexible.

As a result, you can focus on your business’s recovery before you think about repaying the loan.

How do lenders decide whether to borrow?

Direct lenders often specialise in specific sectors – for example, agriculture, automotive, retail, healthcare or real estate.

In any case, when you approach a firm for finance, it will do a significant amount of due diligence to identify whether your business is a ‘good fit’ for its investment.

Generally, there are three key concepts that firms use to assess your business.

EBITDA

A key measure used to gauge a business’s financial performance is its earnings before interest, taxes, depreciation and amortisation (EBITDA).

To learn more about what this is and how it works, read our brief guide to EBITDA for small businesses

Leverage ratios

A lender will use these ratios to determine how much debt your business holds against other measures on your balance sheet.

Most importantly, the debt to EBITDA ratio measures your company’s ability to repay its debts.

A high ratio may indicate that you’re currently too burdened with debt to be able to pay back further loans.

To learn more, read our article: What level of debt is healthy for a business?

Private Credit vs. Private Equity: An Overview

Securities traded on the public markets, like stocks and bonds, may be the backbone of most everyday investors’ portfolios. But there are also plenty of alternative investments that aren’t publicly available, like private credit and private equity.

These assets can be quite profitable, but because they’re also risky and tend to tie up capital for a long time, trading generally takes place among institutional investors and accredited investors.

In the private credit market, investors make loans to businesses and sometimes individuals who may have trouble accessing credit from banks or the public market. Because there is often a heightened risk that the borrower may be unable to repay the loan, private credit investors can collect higher interest rates than they would earn on bonds or other debt investments.

Private equity investing, meanwhile, involves taking an ownership share in a company that isn’t currently traded on the public markets. Unlike a stock, which can be easily bought and sold on a public exchange, private equity investments require investors to make a longer-term commitment with their capital. In exchange for this lack of liquidity, private equity investors also look for elevated returns.

The chance for outsized gains might make private credit and private equity attractive to investors who have access to these private markets.

Pros and Cons of Private Credit Investing

Pros

- Rapid growth of industry

- Predictable returns outperforming other fixed-income options

- Diversification and low correlation with public markets

- Priority for repayment (as creditor) in case of bankruptcy

- Flexibility to manage risk by selecting different types of loans

Cons

- Stringent accreditation requirements and high minimum investments

- Illiquidity

- Increased default risk

- Management fees

- Lack of transparency and regulatory protections

Pros and Cons of Private Equity Investing

Pros

- Rapid growth of industry

- Possibility for huge returns

- Diversification and low correlation with public markets

- Increased control over management decisions

- Potential to benefit from expertise of private equity firm

Cons

- Stringent accreditation requirements and high minimum investments

- Illiquidity

- Management fees

- Lack of transparency and disclosure requirements

- Limited recourse in case of bankruptcy, with chance of losing entire investment

Which Is Better: Private Credit or Private Equity?

Private credit and private equity are both alternative assets that could be attractive to investors looking for different benefits for their portfolios. Private credit may be appropriate for investors seeking relatively stable and predictable returns that often exceed those of bonds and other fixed-income assets. Private equity could be suitable for those in search of high potential returns, although this also means elevated risks.

What Types of Investors Typically Invest in Private Equity?

Private equity often requires a high minimum investment and a commitment of capital for years or even decades. Given these characteristics, private equity firms typically vet investors based on strict accreditation standards. For this reason, institutional investors and individuals with a high net worth or strong financial expertise dominate the private equity space.

Why Is an Investor Likely to Opt for Private Credit Over Private Equity?

Investors may choose private credit over private equity if they are seeking more predictable and stable returns. Because they are acting as creditors rather than equity holders, private credit investors assume lower levels of risk, but their potential profits are limited to the interest generated by the loan.

The Bottom Line: Private Credit

Private credit is a compelling alternative investment that offers several benefits, including income generation, potential return enhancement, and diversification. Unlike private equity, private credit involves non-bank lenders providing loans to small and medium-sized enterprises that are non-investment grade. This sector has grown rapidly due to regulatory changes that have caused traditional banks to pull back from lending to these businesses.

Private credit managers provide direct loans with bespoke terms, typically senior in the capital structure, and charge floating-rate spreads above the reference rate, benefiting from rising interest rates. The primary value-add comes from restructuring expertise rather than involvement in the company’s operations.